May 2025 – Feb 2026

ANZ / Melbourne

Small Business Consultant

Resolving complex client cases in a regulated banking environment, against rising KPI targets.

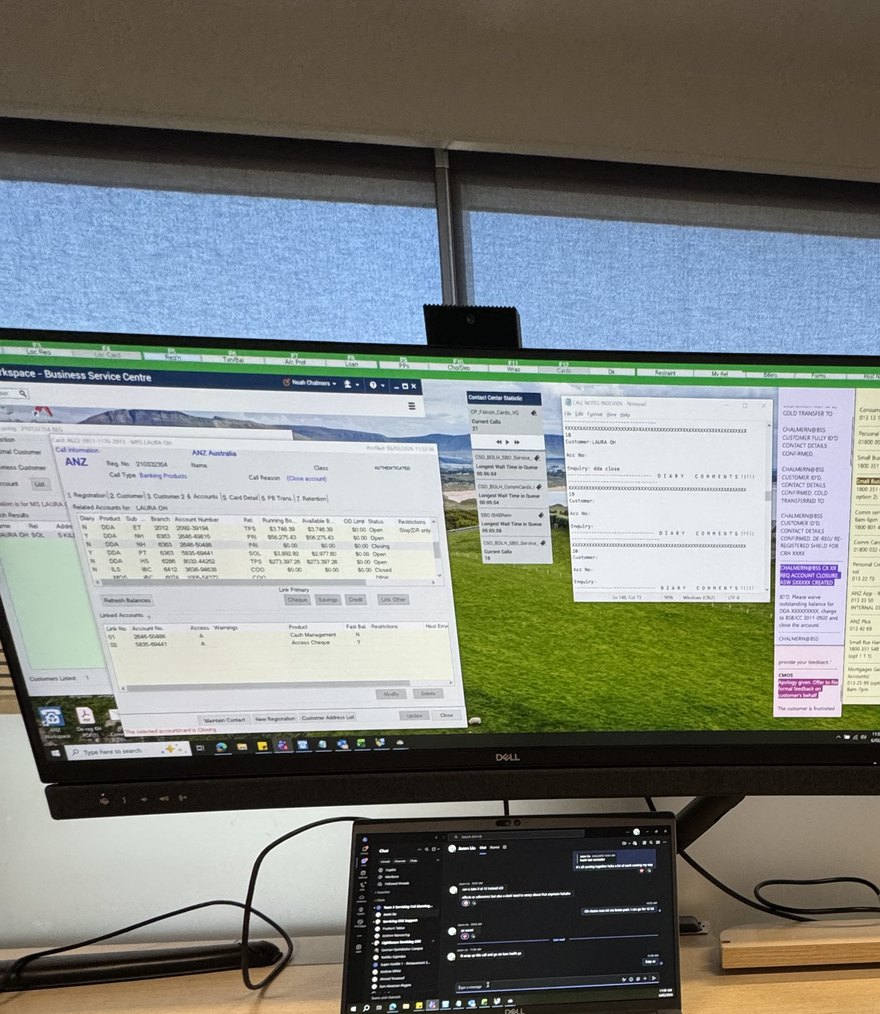

- Managed 45+ client cases daily (peaking at 60), a ~50% increase on the initial 30-case benchmark after targets rose four months in.

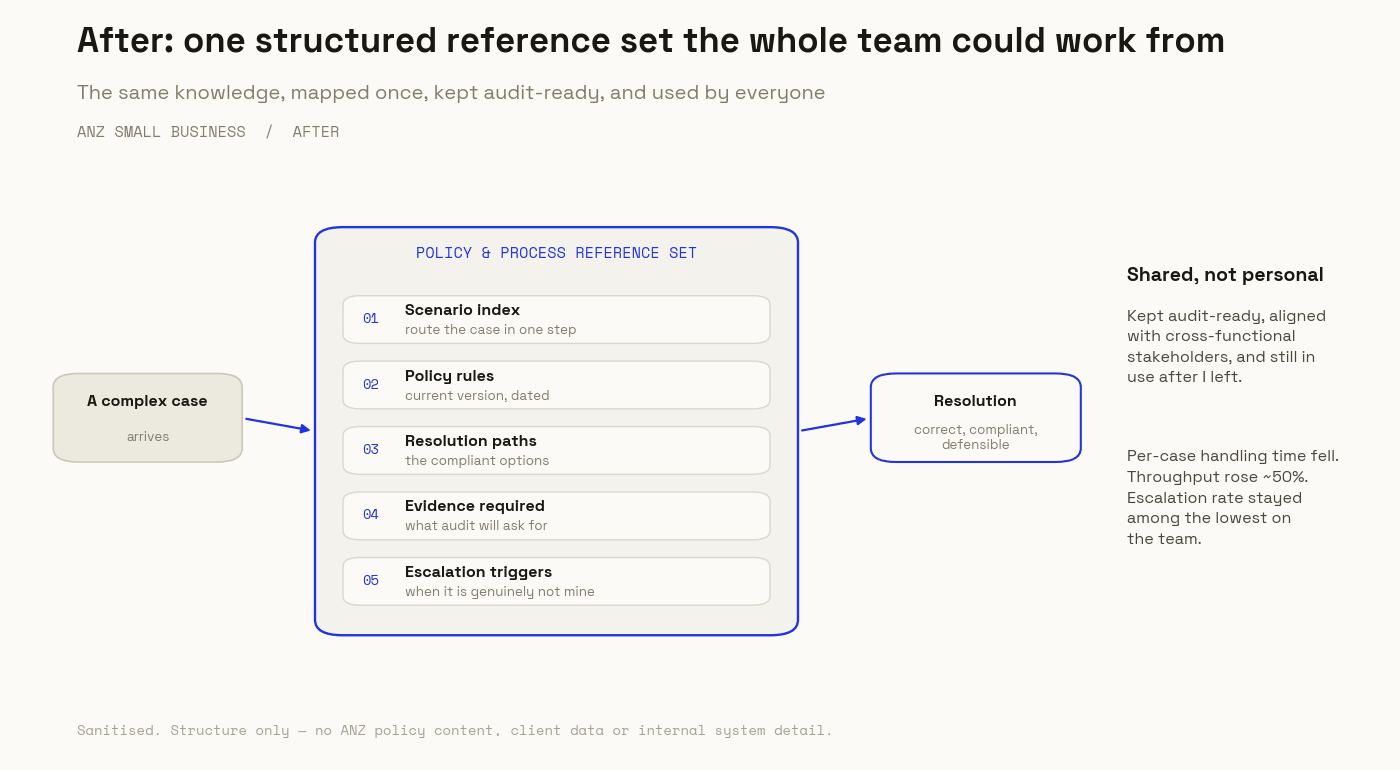

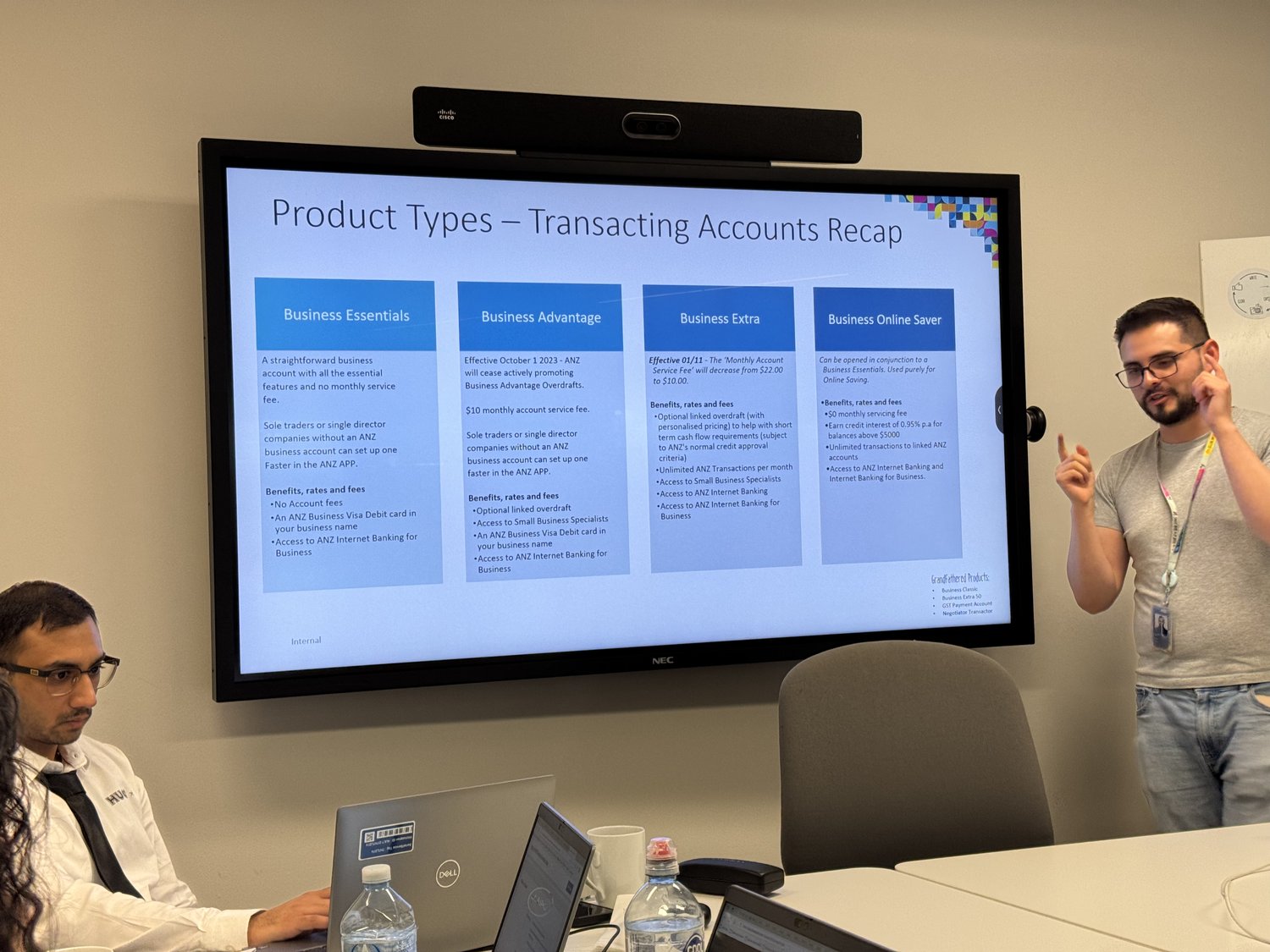

- Built a working reference set of policy and process notes that cut per-case handling time and sharpened call targeting, the main driver behind the higher throughput.

- Held one of the lowest case-escalation rates on the team, independently resolving complex policy scenarios while sustaining accuracy as volume rose.

- Engaged cross-functional stakeholders on compliant resolutions and produced audit-ready documentation of resolution workflows.